How CPP Executives are Manipulating their Benchmarks to Pay Themselves Before Your Retirement

An insider's perspective on the illegitimate $100 million dollar wealth transfer from Canadian tax-payers to CPP execs and employees, and exactly how they covered it up.

As you may have seen, CPP Investments published its Annual Report for the Year Ending March 2026 yesterday.

It would be one thing if CPP was underperforming their benchmark. It would be another if they were manipulating their benchmark to pay themselves unduly. It would be another if they were depressing growth in the Canadian economy writ-large to cover it all up. I’ll prove they are doing all three.

In short, CPP Investments leadership manipulated their benchmarks over 2025 and 2026 to pay themselves and their teams at least an extra $100 million while they missed the baseline target of 4% real return needed to sustain the CPP in the long-term.

Along the way, I’ll reference prior annual reports and my own first-hand knowledge as a former employee to provide you, a government-mandated CPP contributor, with a clear story. A story of how a couple key decisions resulted in the CPP contributing an immense amount of value to Canadian pensioners prior to 2015, and then how its organizational ego got overblown… eventually leading to leadership in 2025 introducing an ill-defined slush fund called the Annual Strategic Objectives Performance Multiplier (henceforth, the “Slush Multiplier”, because I never want you to have to read Annual Strategic Objectives Performance Multiplier again!).

The Slush Multiplier has allowed CPP leaders to increase their compensation and that of their employees in a way that (i) they do not attempt to justify in their annual reporting, and (ii) has no basis in whether they’ve achieved the minimum return hurdle needed to sustain the fund. The introduction of the Slush Multiplier alone helped CPP employees earn over $100 million in undue compensation over the last two years while CPP missed its baseline real return target.

It’s also a story of how CPP leadership in 2025 manipulated the benchmark used by the Federal government (and thereby you) to assess their performance, clouding it in investment jargon so that they can unjustly pocket additional hundreds of millions of dollars of compensation while underperforming their prior standard by hundreds of billions.

I’ll also explain how the funding gap these items created was covered up, in large part, by raising contribution rates on CPP to the tune of tens of billions of dollars each year, directly depressing growth in the Canadian economy.

Finally, I’m going to tell you how it can be fixed, despite CPP Investment’s government monopoly on the pensions of 20-million-plus Canadians.

You may find the explanation for all of this boring, and you’d probably be right, which is why it’s so sinister. I’ve attempted to enliven it. The difference between you receiving what you’ve paid into CPP when you turn 65, or receiving a fraction of what you’re owed today, is reading this and speaking up.

WHAT HAPPENED IN THIS YEAR’S REPORT?

CPP Investments reported an annual return of 7.8% for the year ended March 31 2026. This underperformed CPP’s benchmark return of 13.2% by -5.4%. On assets of ~$700 billion, that reflects $38 billion of ‘forgone’ value last year alone, or roughly $1,000 for every Canadian. Not great, right? But they still grew the fund, you might say! I agree, hold on.

Let’s leave alone that the S&P500 and MSCI World both returned at least 15% over the same timeframe, with the Nasdaq and TSX60 exceeding 25%. But it’s only one year and CPP is a long-term investor, right? I must, again, agree, but tell you I can explain.

Before we start breaking down the fund’s returns over a longer five-year period - the timeframe CPP uses to evaluate itself for compensation purposes - let’s ground ourselves in what the fund paid to its average employee last year.

In 2026, CPP had $2.3-$2.5 billion in non-interest expenses, depending on how you define it, around $1.2 billion of which went to its 2,000+ employees. In totality, CPP salaries were ~0.2% of AUM, versus most large ETFs at <0.1% for total fees. This equates to roughly $500,000 per employee, on average. Now, in years with great performance, you could say CPP employees deserve a huge payday, right? After all, they’d be delivering billions in value to the 20-million-plus Canadians who contribute to the program with every paycheck… right? Again, I agree… assuming they performed.

But, did CPP Investments’ performance over the last five years deserve $1.2 billion in compensation in 2026? Short answer, no. Long answer, buckle up…

COMPENSATION BREAKDOWN

To proceed, we must define specifically how the average CPP investment professional makes their annual half-million. In short, they get a base salary and also a bonus target of between 20-70% of total comp. For a $500,000 take-home, let’s say $200,000 is the salary and $300,000 is the “Bonus Target”. On its own, as finance jobs go, that’s not abjectly absurd. You want to hire good people and pay them handsomely in a way that’s based on performance. There are very few people in the world who can genuinely earn above-average returns on a portfolio year-in and year-out, and when they do it in private industry they get rich. Warren Buffett rich. So to get them to come to your pension fund, you want to pay them very well when they perform. You want to make them not quite as rich as those in private industry, but rich and powerful enough to belong to the same clubs and associations.

Prior to 2025, the bonus target of CPP employees was based purely on performance - one half absolute (e.g., a 7% return) and one half relative (e.g., 7% actual return beat the benchmark of 6% by 1 percentage point). Now, this may not sound problematic theoretically, but if you open the 2024 annual report and go to page 74… you’ll see this became a massive problem for CPP leaders. This Pure Performance Multiplier algorithm spat out a multiplier of 0.62x for the year ending March 2024. Ouch! This is actually a massive problem, not for taxpayers - I mean, yes for taxpayers - but more immediately for CPP leadership and their ability to manage their employees.

Since the performance multiple was 0.62x, an employee making ~$500,000 would receive $186,000 as a bonus instead of his normal $300,000. Even after-tax at the highest marginal rate that difference is at least a year, maybe even two, at Upper Canada College! They might have to go to… shivers… public school! Won’t somebody PLEASE think of the children?!

On one hand, I can empathize with someone thinking they’re going to get $300,000 and getting $186,000 instead. If I employed that person I’d be concerned about being able to continue to manage them. Maybe they’d find a new job. I get that.

With my other, CPP-contributing hand, I’m pulling a Mr. Krabs.

Anyway, CPP leaders saw the incentive problem this created with their employees, and so they resolved to change the compensation structure in 2025. But how? Maybe they could reduce the lookback? Or change how comp was tied to performance? Let’s look at what they actually did.

THE SLUSH MULTIPLIER

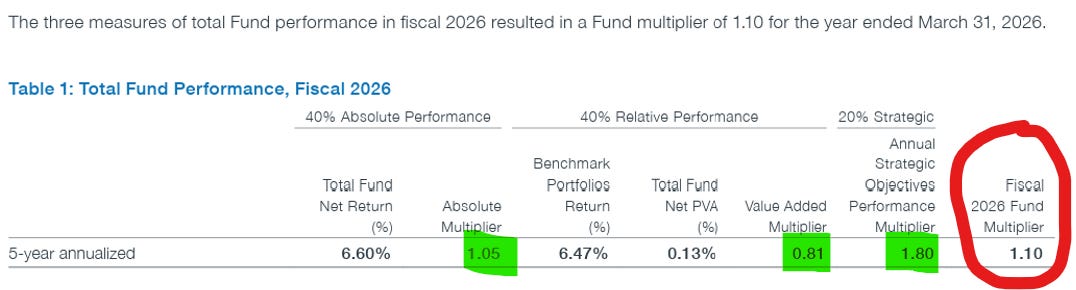

CPP Investments helpfully breaks down their Fund Multiplier calculation for 2026, which spits out 1.10x (ahhh, SO much better than 0.62x!). This is pictured below and can be found on page 82 of the report:

But how did they get from a 0.62x to a 1.10x Fund Multiple in two years? Let me break it down:

40% of the multiplier is now based on Absolute Performance, versus 50% in 2024. On its own, not entirely absurd.

However, CPP employees “earned” a 1.05x multiplier in 2026 for achieving a 6.6% return over the last five years, including inflation, which is actually a pretty huge problem, arguably moreso than anything else I’ll speak to in this entire article.

According to the 2026 Annual Report, the chief actuary of Canada says that the organization must earn an average annual return of 4.0% after inflation to be sustainable, long-term. Inflation in Canada over the last five years was 3.7%, meaning the real post-inflation return of the Base CPP has been 2.9% over the last five years, missing its long-term Chief Actuary target by MORE than a full percentage point. The leaders of the CPP confirm this on page 37 of the 2026 annual report, but inexplicably still give themselves a 1.05 multiplier here.

Moving on for now…

40% is Relative Performance versus 50% before, which still feels mostly appropriate. This earned employees a 0.81x multiplier on their bonuses for being… 0.13% above their Benchmark.

This actually felt kind of punitive to me, and offsets the generous Absolute Performance multiple a bit, so at the risk of over-explaining everything, let me just say, for now, “I’d be OK with this in isolation”. However, it does make me think… why such a low multiple for outperforming your Benchmark?

Combined, this 80% spits out a multiplier of 0.93x. Definitely better than 0.64x, but still not quite 1.10x…

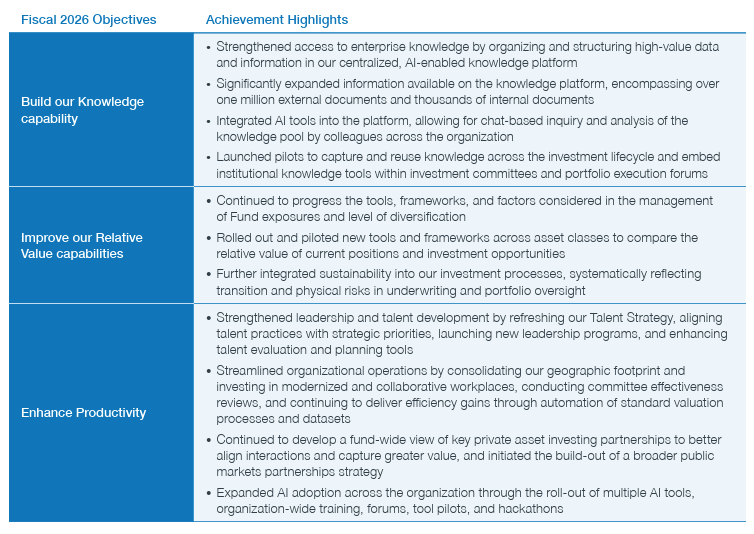

The final 20% of the 2026 compensation algorithm is our Slush Multiplier, established 2025, which is 1.80x. Which… well… like… OK… I guess! Theoretically, it could make sense! It really depends on if there are valuable objectives that the CPP leaders are executing on super well. To give yourself a healthy 1.8x multiplier they must have done a really good job at all the other important objectives they had besides generating returns for pensioners? Maybe they solved world hunger, or unblocked the Strait of Hormuz? Let’s take a look at those all-important strategic objectives:

I mean…I don’t know if that means anything to you but it doesn’t to me! I hope McKinsey was well-paid for that pablum. I want to emphasize that the overall Fund Multiple moved from ~0.9x to 1.1x because of just how well everyone at CPP executed on… checks notes… “refreshing our Talent Strategy”, “piloting new tools and frameworks across asset classes to compare relative value of current positions and investment opportunities”, “Expanding information available on the knowledge platform by one million external documents”, and “Continuing to progress the tools frameworks and factors considered in the management of Fund exposures and level of diversification”. Deep breath.

That move that the Slush Multiplier creates - from 0.93x to 1.10x - represents a transfer from the Canadian taxpayers to CPP Employees to the tune of $50-100 million last year alone, and even more in 2025 when the Slush Multiplier was a whopping 2.0x.

John Graham, President & CEO of CPP Investments, earned ~$7 million on a 1.33x performance bonus (better than the rest of his employees) while underperforming his benchmark. The Board of Directors actually does at least attempt to justify the G-man’s compensation on page 80 of the 2026 report [my emphasis added].

“Our assessment of Mr. Graham for the year reflects several significant achievements, including strong financial performance despite a challenging global environment [STOCK INDEXES WERE UP 15-25%, BUT I GUESS TRUMP WAS A REAL JERK?!]. By also advancing key strategic objectives, Mr. Graham ensured CPP Investments maintained its focus on long-term value during the year [HOW, EXACTLY?!]. The Board awarded him an incentive multiplier of 1.55 [BASED ON WHAT?!]. The weighted average of the Fund multiplier and the department/ individual multiplier resulted in an overall incentive multiplier for Mr. Graham of 1.33 . The Board awarded Mr. Graham total direct compensation of $6,827,644 for fiscal 2026, consisting of salary, an in-year award and deferred awards, as shown in Table 2. Mr. Graham also received standard pension and benefits. [MUST BE NICE!!]”

So, in 2026, the CEO and employees of CPP Investments were judged to have earned their full target bonus and an extra 10% of juice on their bonuses because they did such a good job achieving their vague strategic objectives while underperforming the 4% real rate of return required to keep the CPP in good standing over a generous investment period of five years. Furthermore, the CEO responsible for all this gets an EVEN HIGHER multiplier of 1.55x on his individual performance to get him a $7 million payday.

So, I mean… that’s bad on its own. But that’s it, right? CPP’s leaders solved their employee retention problem with the Slush Multiplier, and we’re just losing a couple hundred million bucks to their North York extensions? Trickle-down economics, right? It’s still good! It’s still good!

Laughs in Orwellian.

Just wait… it gets worse…

A HISTORY LESSON

I got a funny feeling reading the 2026 report, that - regardless of the new, wonky Slush Multiplier - the actual benchmark numbers didn’t quite make sense. Indeed, it seems that CPP Investments retroactively changed how it calculates its benchmark portfolio as of the 2025 Fiscal Year. Review CPP’s 10-year historical returns versus benchmark for 2026 versus 2024 below, and you’ll see that - on the whole - the 2026 Benchmark is substantially easier than the one from 2024.

2026

2024

Before I get into the why, I unfortunately need to take you through the entire history of the organization. It’ll be… relatively quick.

In 2000, CPP Investments was just CPP, and it was managed more like a life insurance portfolio before the Bill Gross era, invested in something like 95% Debt and 5% Equity and employing a few traders to occasionally re-balance the portfolio and stress test it against future cash outflows. Thank goodness this was changed! Our former Prime Minister Paul Martin, the late John MacNaughton and the early teams at CPP deserve all the credit in the world for moving toward a market risk target of 65% equity and 35% debt by 2007. Regardless of the impending 2008 Great Financial Crisis right around the corner, this investment mix decision undoubtedly generated hundreds of billions for Canadian pensioners. Thousands for each and every Canadian.

That said, the 2026 report goes on to say “a targeted risk level of 65% of equity and 35% debt… is in the typical range for conventional fully funded pension plans”. So while this was a great decision, I’d argue CPP Investments simply did the bare minimum here, going from a far-too-conservative position of 5/95 to a more-generally-held-standard of 65/35. It would have been tantamount to malpractice NOT to move to this number, especially with the organization’s unique position of still having decades until it was a net payor of cash.

In 2015, CPP Leadership went further. The Board of Directors approved an increase in market risk from 65% equity / 35% debt to 85% equity / 15% debt, to be phased in over a couple years. CPP Investments also adopted a Benchmark Portfolio against which they’d compare their performance, with 15% weighted toward Canadian government bonds and the other 85% directly tied the “S&P Global LargeMidCap Index”, which is defined as comprising “the stocks representing the top 85% of float-adjusted market cap in each developed and emerging country.”

Another good decision! And this time I’ll say that it wasn’t an obvious one. Many other pension funds across the world held closer to the 65/35 standard, with many still below that equity number today. However, there’s a good reason for that, which is most other pension funds didn’t have the enviable position of being a young fund and projected net receiver of cash for another few decades. CPP Investments takes in funds from its CPP payroll taxes which it uses to invest and will eventually use to pay retirement benefits. US Social Security, Ontario Teachers, OMERS, the Japanese Pension fund, and CalPERS, are all net payers of cash, relying on their investment returns to fund immediate payments. If you look at CPP Investment’s relative returns and compare them to other pension funds across the world, CPP has routinely outperformed, but it does so because of the structural advantage of being able to move to an 85/15 equity/debt split as a result of being a net receiver of cash rather than net payer. The leadership at the time, led by Mark Wiseman, current ambassador to the US and former Blackrock philanderer, was smart not to ignore this.

From this point forward, government bonds returned somewhere in the 1-2% range while S&P Global LargeMidCap Index returned in excess of 13%, compounded annually, dividends reinvested. The decision to go from 65/35 to 85/15 generated additional hundreds of billions for Canadian taxpayers and should also be applauded.

I still remember in 2014, diploma from Queen’s still available for download from the student portal, when Mark greeted me and 30 or 40 other smart young minds who were joining CPP Investments for the first time.

See, I fell into finance because I was smart, and I thought it was more interesting than being an accountant. I ended up joining the firm because my alternative was being an investment banking analyst - which sucked and continues to suck - and back in those days Private Equity funds hadn’t started reaching out with 24-hour exploding contracts in the six figures to burgeoning senior kindergarteners with 99th-percentile paper-cutting skills. Basically, there are two broad categories of Finance Jobs: sell-side, which is investment banking (again, sucks) or equity research; and buy-side, which basically involves working for “A Couple Rich Investor Dudes”, either at a private equity fund or a public company.

I liked that I was venturing out into the real world with the mission of earning money for hard-working Canadians who trusted this money to be there for them. Better them than ACRID.

And so, I sat in a meeting room on the 19th floor of Two Queen West. It was in the kind of meeting room that has siblings in virtually every other towering office building in the downtown Toronto core dated to roughly my birthyear. Large banquet halls in the sky with floor-to-popcorn-ceiling windows offering glimpses of Lake Ontario between the other skyscrapers, each probably containing similar rooms though their windows were tinted so I couldn’t be too sure. The room could be divided by these giant movable accordion partitions covered in the same soft fabric as the floor, presumably for acoustics. They had been extended so that the room was divided into the correct amount of space for the number of us in attendance.

Mark started by reminding us that accepting gifts over $100 was reason for a written warning or even an immediate termination without cause, and talked about the opportunity we had to make life better for Canadian taxpayers and the trust that they were placing in us. The second statement justified the first, and we would take it to heart for a while as we watched all our ACRID-backed friends get taken out to Leafs games. I was a Sens fan anyway, I told myself.

Mark told us that the penalty for breaching Canadians’ trust, collectively as an organization, was that we would be replaced with three guys in a windowless basement rebalancing the 85/15 index. At the time, to a type-A kid just out of school with something to prove, I took that as a threat. A threat that I didn’t have anything to offer, to the profession or to the Canadian taxpayer. That my four years at one of the finest business schools in Canada had been a waste. It was intended as such, and it was the right threat for him to make.

Then, Mark broke out a chart in which he showed that if CPP Investments continued at its 65%-equity/35%-debt split, we could maybe earn a 3.5-4.0% real rate of return. However, if we took on more risk as a maturing organization, by moving to 85/15, we could earn a 4.0-4.5% real rate of return and be able to reduce contributions in the future. Indeed, the 2019 annual report makes reference to this:

When assessing the sustainability of the CPP, the Chief Actuary assumes a long-term net annual return averaging 3.9% after inflation. If through active management, we could consistently deliver returns averaging 0.5% a year higher, then:

The minimum contribution rate could eventually be reduced from 9.79% of covered earnings to 9.43%.

That is equivalent to a combined savings to employees and employers of more than $1.7 billion annually at current earnings levels.

Alternatively, the additional returns could be used to increase benefits or held in reserve to strengthen the sustainability of the CPP.

But wait, you’ll ask, isn’t the current contribution rate 11.9%, a full 2+ percentage points higher than the 9.79% they reference? And don’t I also have to contribute 8% if I earn more than $75,000 when I didn’t have to before 2019? The answer to both of those questions, simply, is yes. Later that same year, CPP rates would be increased, the name changed to CPP1 or Base CPP, and CPP2 or Additional CPP was introduced on incomes above ~$75,000.

The stated reason was to bolster Canadian retirement incomes: 25% of average income was insufficient to provide for the average Canadian in retirement. I can’t say I whole-heartedly disagree with that statement, but who made that decision and why? Especially when earlier that same year CPP was talking about reducing CPP contributions for the benefit of the Canadian economy, which was never discussed again.

I’ve been told from sources that - if you speak to anyone senior in the organization in 2019 who actually knew what was going on - CPP Investments had accidentally over-extended itself around this time. It had made too many non-cash-flowing and illiquid investments and would either have to sell equities or raise more cash in order to pay its near-term cash outflows. Now, none of this was going to have to happen immediately, but the Chief Actuary would have had to talk about the impact in their next report, and selling equities would have “piled on” to the issues within said report. To explain that in slightly more detail, when you remove equities from the portfolio to pay for immediate liquidity needs, that creates a much larger gap in 20-30 years because you’ve lost an asset that would have returned 8-12% over the next 20-30 years. You and I don’t see this clearly in the reporting but the Chief Actuary would have.

There was an exodus of senior leaders during this time, which you can track, and if you ask the junior folks, the fund stopped doing deals for a while in many of its groups. Of course, it couldn’t stop entirely or it would be too obvious. The answer was to do fewer deals while tapping the Canadian tax payer for incremental CPP1 contributions AND incremental CPP2 contributions.

The cost of that answer, based on extrapolating the never-realized savings from the 2019 Report, would tell us that CPP has increased its drain on the Canadian taxpayer (split between employer and employee EVENLY) by $10 billion annually since that time. That’s $125 out of the pocket of the average Canadian, every year, and $125 out of the pocket of every employer for each full-time worker in its employ.

The CPP’s historical journey from 2000 to 2015 to move from a 5/95 portfolio to an 85/15 portfolio was very positive. We, as Canadians, can rightly be proud of the CPP and its leaders during this time, and of the decision-making that led the organization there. But that all happened over a decade ago. I’m not here to argue the history or whether CPP Investments has contributed positively to Canadians as a whole. It undoubtedly has.

I’m asking… WTF has been happening in the last few years?!

INTO THE WILDERNESS

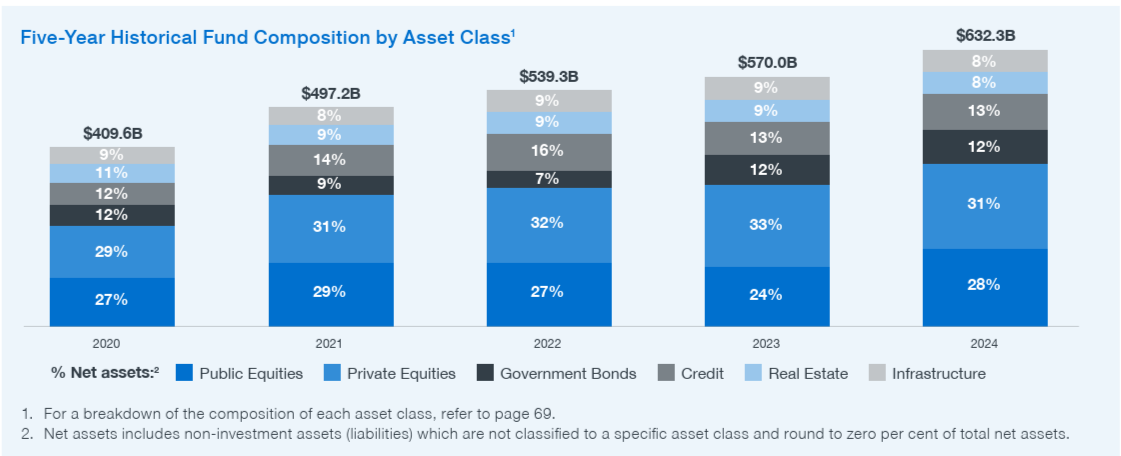

From 2015 to 2025, CPP Investments used a benchmark of 85% S&P Global LargeMidCap Index to reflect the equity part of its returns and 15% in a Canadian Government Bond Index to reflect the debt part. To me, this makes a lot of sense. Easy and simple to understand, this benchmark also has the benefit of fairly accurately reflecting the types of assets the fund held, as you can see in the chart below. This is especially the case if you assume that Infrastructure, High-Yield Credit, and Real Estate are more reflective of equity returns over time than debt. I think there’s some nuances there I can’t get into here, but overall I’d agree with that assessment. If you argued for a more lenient 80/20 or 75/25 benchmark rather than an 85/15 based on this fact, you could convince me. I’d get on board. Overall, that would feel right to me!

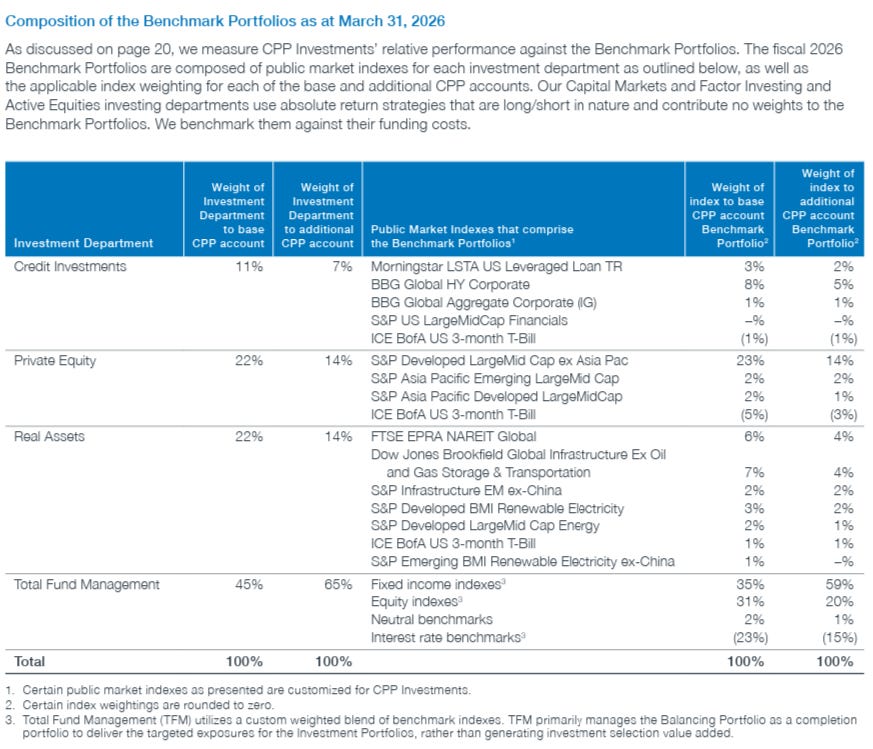

So what did CPP Investments change their Benchmark to in 2025? Let’s take a look!

I mean… I don’t know what to do with that. I’m a CFA and an investment professional who should be able to interpret this, and I have NO FREAKING CLUE what to do with that.

What I can tell you - and this is the upshot - is that based on CPP Investment reporting, the “revamped” 2026 Benchmark Portfolio returned 8.1% over the last five years.

The Benchmark Portfolio CPP Investments would have had to use if they hadn’t changed it in 2025? That lovely… simple… beautiful… 85/15 index that I used to know like Gotye… returned 11.6% annually over the same five years. I don’t know what that 40% Relative Performance multiplier would be for underperforming that index but I bet it’s a lot lower than the 0.81x that got used for 2026.

Let’s reframe those numbers another way though. CPP Investments had ~$400 billion in assets in March 2019, so if they had simply invested 85% in their equity benchmark (”S&P Global LargeMidCap Index” yielding 13.3%) and 15% in Canadian Government Bonds yielding a conservative 1% over the last five years… CPP Investments would have an incremental $140 billion in returns over those five years versus what they actually earned, with no incremental CPP1 or CPP2 contributions required. That’s an extra $3,500 in each Canadian’s pocket.

To put that yet another way, if CPP Investments had actually invested 58% of its funds into the LargeMidCap Index at 13.3%, and the other 42% in Canadian Bonds at 1%, it would have done just as well as the 2,000+ employees at CPP Investments actually did. Read that again.

For the inclined among you, I asked ChatGPT and Gemini… and they both said if your active manager can’t beat a 75/25 index, you should get rid of them and invest passively! That matches my gut. CPP Investments is at 58/42.

CPP Investments gave themselves the Slush Multiplier to try to pay themselves more, but it wasn’t enough, so they had to adjust their relative benchmark too.

SO WHAT DO WE DO?

Well, first, you can get upset. No, but really. Share this and maybe it’ll get around. Send it to your representatives. The Globe and Toronto Star both had articles on this yesterday with broadly similar takeaways, but their articles are behind paywalls and don’t have the whole context. To change the charter of CPP Investments requires a 2/3rds vote of the Canadian senate representing 2/3rds of Canadian provinces. It’s very hard to do! The only way for it to change is general public outcry.

I know how CPP Investments works. There are hundreds of people there (maybe dozens) who are concerned about the future of the average Canadian’s retirement in the same way I am; they are people still not accepting that $100+ gift from a client because they want your trust. There are hundreds more just keeping their heads down and pretending - to others and themselves - not to hear the loud sucking sound their employer is making at the roots of the Canadian economy. These people are - mostly, like any group of people - good at their core. I’ve enjoyed a beer or two with many of them. However, the only way to effect change is for the 20-million-plus Canadians who contribute to the fund, as well as those inside it, to demand transparency and accountability. For our benefit, our children’s benefit, and for the employees, because living in the Orwellian nightmare of CPP Investments is not healthy for them either. But hey, that’s just, like, my opinion, man.

You can share this and we can collectively demand that the CPP leaders do some combination of: (i) become more transparent rather than less, and (ii) shift to a less-expensive form of asset management largely focused on passive index investing... over time. I’m not saying they have to do it tomorrow, as that also involves risk. There are also a variety of ways to accomplish it. We could cap CPP Investment’s expense ratios below current levels in a graduated manner to “force” a move toward passive indexing in a similar way to how one might dollar-cost-average into the market. We could also demand more clarity on compensation calculations, like the 1.8x Slush Multiplier and the 1.55x individual performance multiplier

While I find CPP’s performance lacking versus the market, that’s actually not my chief issue with the report. If they were honest about their performance and didn’t introduce the Slush Multiplier, I wouldn’t have been able to write this article. The reality is that CPP Investments’ leaders adjusted their benchmarks and introduced a Slush Multiplier to increase their own compensation and make it easier for themselves to manage employee turnover, while failing to meet the minimum real return of 4% required by the Chief Actuary over a significant period of five years. In doing so, they put themselves before your retirement.

If CPP’s leaders really cared about their professed purpose at the top of the 2026 Annual Report to “help provide a foundation for more than 22 million Canadians to help build their financial security in retirement” - tough tagline by the way, use a thesaurus - they’d be honest in their reporting and we could have a real conversation about them reducing their active management of investments, over time. They can’t beat the index, and Canadians shouldn’t give them more time to try.

Looking forward to any feedback and answering any questions. If you’d like to understand but don’t, shoot me a message… I probably just explained that part poorly.

EDIT:

I have to come clean, I wish I’d included this in my original piece... I would like to say that this all comes from a place of love, for the taxpayer and the employee at CPPIB. I don’t think they should all lose their jobs nor a majority of them nor should we move to a passive index tomorrow. What’s life without a little mystery, though?

Edit2: This guy Steven Adang did a smart thing comparing the CPP benchmark to other indexes and also demanding increased transparency. I thought it was neat! FLARE™ Risk Intelligence

Former MF industry insider here. Insiders are always going to use the benchmark that makes them look better. It’s not concerning to if CPP made their BM more reflective of the actual strategy. It makes sense for the “global bond” sleeve to be BM’d against the Bbg Global Agg etc. But the fact that they back-dated the BM is concerning. Doesn’t sound like much oversight is needed there it doesn’t even look like they needed to disclose specific benchmarks (I didn’t see that they did in the 2024 report at least).

When we changed the BM we needed to clearly state what it was, when it was changed, and what the new one is.

Anyways. Great read keep up the good work.

Great work Matt. Expose the truth!